You are now subscribed

Your newsletter sign-up was successful

Want to add more newsletters?

Twice daily

MoneyWeek

Get the latest financial news, insights and expert analysis from our award-winning MoneyWeek team, to help you understand what really matters when it comes to your finances.

Four times a week

Look After My Bills

Sign up to our free money-saving newsletter, filled with the latest news and expert advice to help you find the best tips and deals for managing your bills. Start saving today!

The housebuilder's profits are booming, but there's still a bit more to go for, says Phil Oakley.

Britain's housing market is in rude health. In London and the southeast of England it is positively booming. So it's not surprising that housebuilding companies, such as Bovis, are reporting stonking increases in their profits and dividends.

The government's Help To Buy scheme (which provides taxpayer guarantees on mortgages to encourage banks to lend) is effectively underwriting a significant chunk of demand for builders of new houses, and this does not look like it will end anytime soon.

MoneyWeek

Subscribe to MoneyWeek today and get your first six magazine issues absolutely FREE

Sign up to Money Morning

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

However, the shares of housebuilding companies, like the market they operate in, have a tendency to move from boom to bust. The recessions of the early 1990s and late 2000s wrought havoc with their profits and finances. Shareholders were frequently asked to cough up more money to put them back on an even keel.

These painful experiences should have taught investors in housebuilders some valuable lessons. They are not shares to buy and forget about, where you can simply sit back and reinvest your dividends and see your wealth compound. On the contrary these are trading stocks.

Although the managers of these companies say they can effectively manage the ups and downs of the housing-market cycle, history suggests that despite their best intentions, they can't.

Yes, they may be able to stop their companies from going bust but you should expect that the future has a good chance of being somewhat similar to the past and that profits will move up and down a lot. So from time to time, investors in housebuilders need to get involved in a guessing game.

You have to work out when to buy and when to sell. So is there any money left to be made here? Or should you steer well clear of the shares?

The outlook

Opinions on the outlook for house prices are ten a penny. Trying to predict them is not easy. All I'd say is that, relative to wages and rents, they don't look particularly affordable. If they were, then schemes such as Help To Buy wouldn't be needed.

Builders do have some influence over the prices they receive for example, they can sell more higher-priced family houses, instead of flats, as Bovis is doing. However, other than that, they have to rely on the general strength, or otherwise, of the overall market.

But where housebuilders can add real value is in where they build, and how much they pay for land. If you need a reason to be bullish on the outlook for Bovis and its shares, then its land-buying skills could hold the key to higher profits and returns on capital employed (ROCE). This, in turn, could lead to higher dividends and a higher share price.

Bovis has a land bank of 17,702 plots,all of which have planning consent.It has added 4,600 new plots this year. When working out what to pay for land, builders work backwards from the expected selling price of the properties they aim to build on that land.

Bovis reckons that on its newly acquired land, it will get a ROCE of between 25% and 30%, which would be very impressive.

Then there's the company's strategic land bank of 19,608 plots, which do not yet have planning permission. This can be bought far more cheaply than consented land, with the hope of a big rise in value when, and if, planning permission is eventually granted.

A full three-quarters of Bovis' land is in the southeast of England, where demand is high especially for family houses.

Bovis is confident that it can ramp up the rate at which it builds new houses from around 3,650 properties in 2015, to between 5,000 and 6,000 in a few years from now.

As long as house prices remain relatively steady, then this big increase in building will feed through to a large jump in Bovis' revenues. Not only that, but with the prices the company has paid for land already known, Bovis expects to see profit margins and ROCE increase significantly.

During the last year, Bovis' ROCE has been 13.4%. It expects this to rise to 16% by the end of this year, and to reach at least 20% by the end of 2016.

If Bovis can do this, then its profits and dividends are going to be a lot higher than they are at the moment. The dividend payout for this year will almost triple to 35p per share, and will be at least that level in 2015 as well, which gives the shares a decent yield.

If the market remains healthy, then investors can also expect to see bonus payouts on top of the regular dividend.

Is there anything left to play for?

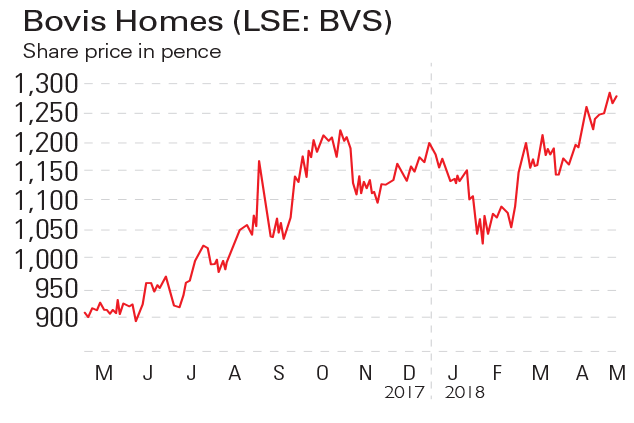

The share price is up by just over 6% this year, after making very strong gains in 2013. City analysts expect Bovis to deliver after-tax profits of just over £100m this year that's about 25% below its peak profits during the last cycle, after adjusting for inflation.

People are rightly wary about the sustainability of Bovis' profits. And it's true that a multiple of 1.3 times its net asset value (NAV) is no bargain. But if Bovis can ramp up production in a benign market, then its profit momentum may attract fresh buyers. The bull market in houses and housebuilders' shares may still have some way to run.

Verdict: a speculative buy

Bovis (LSE: BVS)

Directors' shareholdings

-

ISA fund and trust picks for every type of investor – which could work for you?

ISA fund and trust picks for every type of investor – which could work for you?Whether you’re an ISA investor seeking reliable returns, looking to add a bit more risk to your portfolio or are new to investing, MoneyWeek asked the experts for funds and investment trusts you could consider in 2026

-

The most popular fund sectors of 2025 as investor outflows continue

The most popular fund sectors of 2025 as investor outflows continueIt was another difficult year for fund inflows but there are signs that investors are returning to the financial markets

-

Why you shouldn't pay full-price for a shoddy new-build house

Why you shouldn't pay full-price for a shoddy new-build houseFeatures Housebuilder Persimmon is to allow buyers to hold back some of the purchase price of their new-build home until problems are resolved. It's a start, but it's hardly revolutionary.

-

If you'd invested in: Bovis Homes and Crest Nicholson

If you'd invested in: Bovis Homes and Crest NicholsonFeatures Regional housebuilder Bovis has seen its shares rise by 40% in the last year, while Crest Nicholson's have slid by 20%.

-

Sharks circle Bovis

Sharks circle BovisFeatures Bovis’s rivals are trying to make a meal of its assets on the cheap. It should hold out for a better deal, says Ben Judge.

-

It’s time to sell out of the housebuilding sector – here’s why

It’s time to sell out of the housebuilding sector – here’s whyFeatures Shares in housebuilders have done very well in the last few years. But it's time to sell. Ed Bowsher explains why, and picks a more attractive sector to buy.