Inheritance tax bills are set to rise – will you be caught out?

The number of people who actually pay inheritance tax is very small. But more and more estates are set to be dragged into its net, says David Prosser. And that could include you.

You are now subscribed

Your newsletter sign-up was successful

Want to add more newsletters?

Twice daily

MoneyWeek

Get the latest financial news, insights and expert analysis from our award-winning MoneyWeek team, to help you understand what really matters when it comes to your finances.

Four times a week

Look After My Bills

Sign up to our free money-saving newsletter, filled with the latest news and expert advice to help you find the best tips and deals for managing your bills. Start saving today!

Inheritance tax is very likely the most hated tax in Britain. And yet, it’s not actually paid by that many people. Roughly 4% of deaths in the UK result in an inheritance tax bill. Just over 24,000 families paid the tax in the 2017-2018 financial year, the last year for which official government statistics are available.

The number may even have fallen a little since then: in 2019-2020, inheritance tax receipts totalled £5.2bn, says HM Revenue & Customs, a 4% drop on the previous year.

MoneyWeek

Subscribe to MoneyWeek today and get your first six magazine issues absolutely FREE

Sign up to Money Morning

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

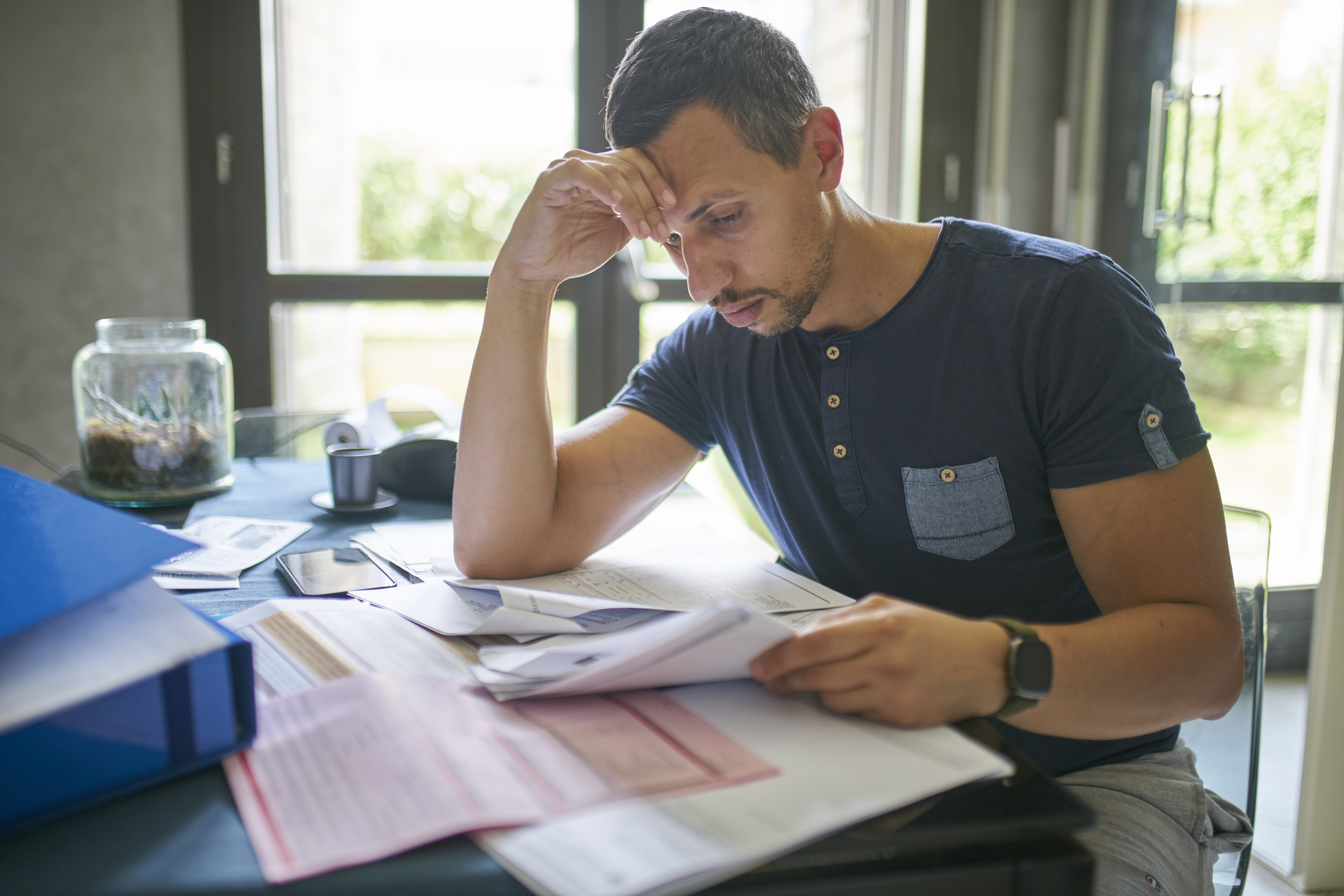

More and more estates will be dragged into the inheritance tax net

Clearly, inheritance tax (often abbreviated to IHT) is an emotive subject. IHT is often described as a “death tax” – dealing with HMRC is the last thing anyone needs following a bereavement.

Many people also feel deeply unhappy about the idea of handing over a slice of the wealth they have built up over a lifetime to the tax office rather than to their families, particularly as they are likely to have already paid significant amounts of other taxes on this wealth.

And while few families pay it, for those who do, the bill is often sizeable. In 2017-2018, the average liability was around £197,000. Many families struggle to pay such large bills out of their more liquid assets, and are therefore forced to make some difficult decisions – such as selling a family home they had hoped to keep, for example.

But perhaps a more important factor for those who aren’t sure whether IHT is something they need to consider or not is this: while IHT receipts have been falling in recent years due to changes that have allowed people to pass on more property wealth to their heirs, this trend looks set to reverse.

The Office for Budget Responsibility predicted in December that the Covid-19 pandemic might lead to a 20% increase in the number of families facing IHT bills, since many deaths during the crisis were unexpected, and therefore unplanned for. And in the longer term, rising property prices look set to drag more families into the IHT net.

Even before chancellor Rishi Sunak’s 2021 spring Budget, the number of people expected to pay IHT over the next five years was expected to rise, with official projections that the tax would raise £6.3bn by 2023-2024, up roughly 20% on five years previously.

The chancellor’s announcement of a freeze in the IHT threshold at current levels until at least 2025-2026 will only increase this number. The Treasury’s own figures show that Sunak expects to raise £1bn in extra IHT over the next five years thanks to this move. So while it’s true that IHT will remain a levy that the majority of people never have to pay, the proportion of estates that incur it will just keep growing.

The good news is that even those families who do face a potential liability, can take perfectly legal steps to reduce the final bill, or even avoid it altogether. The key is to ensure you understand how the tax works, and to plan ahead.

Inheritance tax: the basics

The basic rule is that IHT is due on estates (basically, everything you own, with a few exceptions) worth more than a set amount.

The first slice of your estate is covered by the “nil-rate band” – currently £325,000 – and is completely tax-free; this is the threshold that the chancellor froze in the budget (indeed, it hasn’t been increased since 2009). Your heirs are then required to pay tax out of the estate on its value above this threshold, currently at a rate of 40%.

However, there are some important exceptions to the rule. First, your spouse or civil partner never has to pay IHT when inheriting your estate. Couples are instead allowed to pool their nil rate bands. This effectively enables them to leave £650,000 of assets to heirs with no tax to worry about.

Also, your home is treated slightly differently for IHT purposes. You get an additional “main residence band” covering your home. This effectively raises the total nil-rate band for many people to £500,000 – and so to £1m for couples.

The main residence band was phased in between 2017 and 2020. This is why IHT receipts have – unusually – been falling during that period (and why they’re likely to start rising again from now on, now that the change has fully bedded in).

To establish whether your family might have potential IHT liabilities to plan for, you need to value your estate. Broadly speaking, this consists of everything you own (with a few exceptions), less everything you owe. What you own includes the value of your home, assuming you own it; all your personal possessions; your savings and investments, including those which are free of other taxes such as individual savings accounts (Isas); and any money owed to you, such as pay not yet received for work done or pensions paid in arrears.

For anything you own, or own jointly, you just count your share – if you are married or in a civil partnership, this is assumed to be 50%. A few types of wealth are not usually part of your estate, including life insurance policies and pension savings (more on that later on).

Once you have a total value for your wealth, subtract any debts outstanding, such as mortgage borrowing still to be paid off, outstanding credit card balances and personal loans. Bills also count, as does any income tax you owe.

At the end of this process, you should have a reasonably accurate estimate of the current value of your estate – and whether it exceeds the £325,000 nil rate band, or the £500,000 threshold if you own your home (and it meets a few other conditions – we’ll cover those in the next section). Couples need to test against the £650,000 or £1m combined thresholds.

However, do not forget that the value of your assets – particularly your home, savings and investments – is likely to rise in the years to come, and your debts should fall. As a result, IHT may become an issue even if it is not a concern today. But armed with the figures, you can think about any steps you need to take to head off future problems.

This is the first part in a series on inheritance tax. For the full report and more, subscribe to MoneyWeek magazine and get your first six issues free – sign up here today.

-

MoneyWeek Talks: The funds to choose in 2026

MoneyWeek Talks: The funds to choose in 2026Podcast Fidelity's Tom Stevenson reveals his top three funds for 2026 for your ISA or self-invested personal pension

-

Three companies with deep economic moats to buy now

Three companies with deep economic moats to buy nowOpinion An economic moat can underpin a company's future returns. Here, Imran Sattar, portfolio manager at Edinburgh Investment Trust, selects three stocks to buy now

-

Two million taxpayers to be hit by £100k tax trap by 2026/27

Two million taxpayers to be hit by £100k tax trap by 2026/27Frozen thresholds mean more people than ever are set to pay an effective income tax rate of 60% as their earnings increase beyond £100,000. We look at why, as well as how you can avoid being caught in the trap.

-

13 tax changes in 2026 – which taxes are going up?

13 tax changes in 2026 – which taxes are going up?As 2026 gets underway, we look at what lies ahead in terms of changes to tax rates and allowances this year and how it will affect you.

-

How to limit how much of your Christmas bonus goes to the taxman

How to limit how much of your Christmas bonus goes to the taxmanIt's Christmas bonus season but the boosted pay packet may mean much of your hard-earned reward ends up with HMRC instead of in your pocket

-

Over 1 million pay 45% rate of income tax as fiscal drag bites

Over 1 million pay 45% rate of income tax as fiscal drag bitesHundreds of thousands more people are being pushed into the additional rate tax band by fiscal drag

-

'I've used my annual ISA allowance. How can I shield my savings from tax?'

'I've used my annual ISA allowance. How can I shield my savings from tax?'As millions face paying tax on savings interest, we explore how to protect your money from the taxman. If you've used up your ISA allowance, we look at the other tax-efficient options.

-

Simple assessment explained as millions brace for unexpected tax bills

Simple assessment explained as millions brace for unexpected tax billsIncreasing numbers of people could get letters from HMRC saying they owe more tax due to frozen thresholds, under a system known as simple assessment. Here is what it means for you.

-

What are wealth taxes and would they work in Britain?

What are wealth taxes and would they work in Britain?The Treasury is short of cash and mulling over how it can get its hands on more money to plug the gap. Could wealth taxes do the trick?

-

When is the self-assessment tax return deadline?

When is the self-assessment tax return deadline?If you are self-employed, rent out a property or earn income from savings or investments, you may need to complete a self-assessment tax return. We run through the deadlines you need to know about