The trouble with "World" stockmarket indices and how to fix them

Indices such as the MSCI World or the FTSE World are not an accurate reflection of the global economy

If you have no strong views on where to invest, a cheap passive fund that tracks the whole market is a sensible place to begin. So to build a global portfolio of equities, the obvious starting point is an index such as the MSCI World and the FTSE World. But when you look at the details of these indices, you might wonder if they accurately reflect where you want to invest.

Take the enormous weighting in US stocks, for example (64% of the MSCI World). Or the absence of any emerging markets (EM) – nothing at all in the MSCI World, which is developed markets (DM) only, and only a small part of the MSCI AC World (China, the largest, is just 4%). You may feel that neither of these are consistent with how the global economy works.

Yesterday’s economy

And you’d be right to question that. The US accounts for around 25% of global GDP, while EMs comprise about half. This is not yet reflected in global market indices, partly because DMs tend to have larger and more liquid stockmarkets: more firms are listed, and the free float (shares that are not owned by governments or other controlling shareholders and are available for investors to buy) is typically much higher. But it is also due to valuations: the US now dominates global indices partly because valuations there are so high.

Try 6 free issues of MoneyWeek today

Get unparalleled financial insight, analysis and expert opinion you can profit from.

Sign up to Money Morning

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

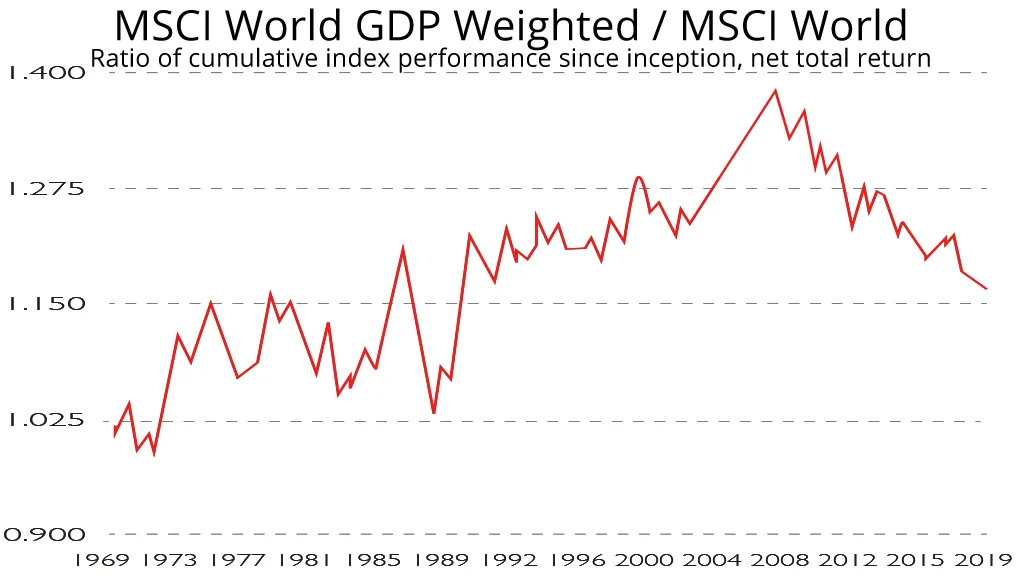

To get a benchmark more in line with the size of the global economy, we could weight by GDP instead. Would that improve performance? MSCI calculates a GDP-weighted index version of both the MSCI World and the MSCI EM. The EM one has beaten the standard index by 1.7 percentage points per year since 2000. The DM one is still ahead overall since its inception in 1969, but has lagged badly over the last ten years because the US beat other developed markets by a large amount over that time. That may continue – but the example of Japan in the late 1980s (when it briefly accounted for more than 50% of global market capitalisation) suggests it could one day reverse dramatically (see chart above).

GDP weighting wins out

If so, GDP weighting could again be better than market-weighting. There are no broad GDP-weighted ETFs – a fund with such poor performance over the past decade would be tough to launch. But a handful of regional funds would build something similar. For example, with five Vanguard ETFs – FTSE North America (25%), FTSE Developed Europe (25%), FTSE Japan (7.5%), FTSE Emerging Markets (37.5%) and FTSE Developed Asia Pacific ex Japan (5%) – you could get most markets closer to their GDP weights, at a total annual cost of 0.18%.