Growth or value investing: which is best?

Ed Bowsher looks at the differences between value investing and growth investing, and which approach is best for investors in 2014.

There are lots of different approaches to investing in the stock market. Some investors focus on dividends, some on patents, others on a whole host of other factors.

But two of the most widely followed approaches are growth and value investing. Put simply, growth investors are looking for the Microsofts and Googles of the future while value investors are looking for stocks that just look cheap.

In this video I take a closer look at how value and growth investing differs, and which approach is best for investors in 2014.

Try 6 free issues of MoneyWeek today

Get unparalleled financial insight, analysis and expert opinion you can profit from.

Sign up to Money Morning

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Transcript

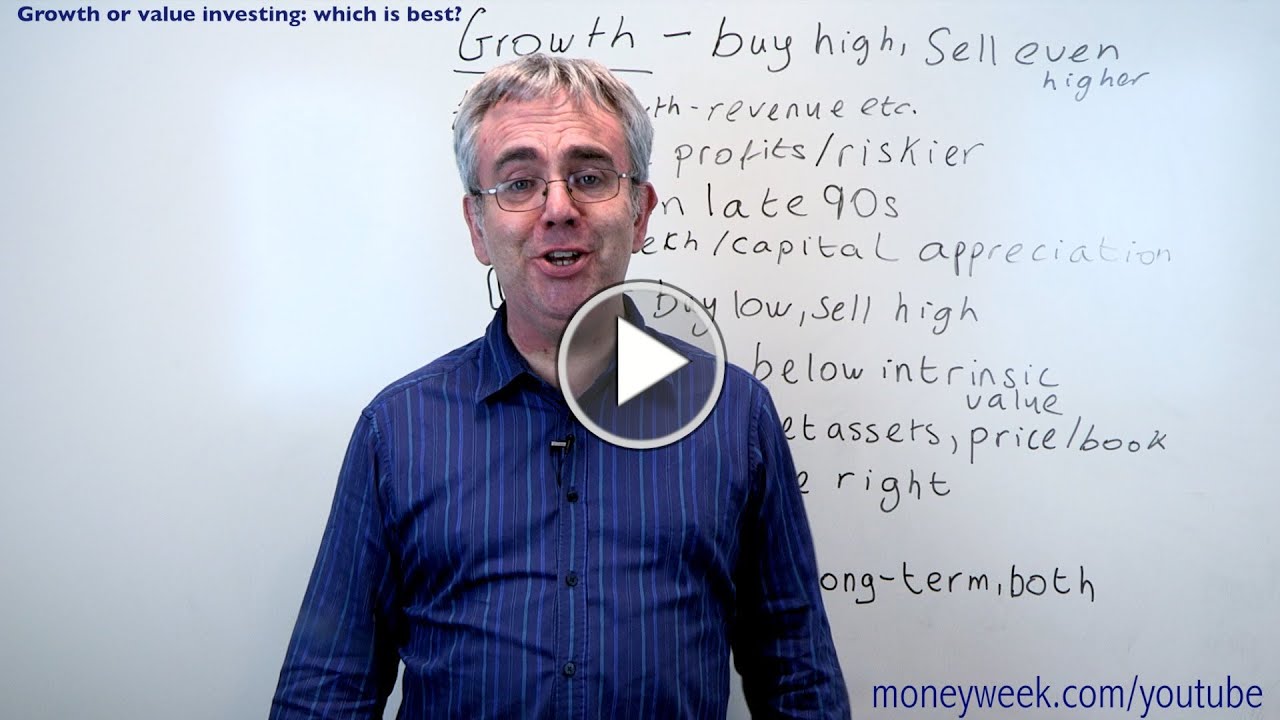

What is growth investing?

So, when you're looking at that growth, when you're trying to measure that growth, you're going to look at things like profit, cash flow, and above all else, revenue. In fact, some growth companies won't even be making profits or generating cash flow. That doesn't matter. If you can see fast growth on the revenue line, you may decide it's worth investing. A few years down the line, the profits and the cash flow will come, share price will go up and you'll make a nice big profit.

Another characteristic for growth companies is if they are making profits, they typically reinvest most or all of those profits back into the business. The management of a growth company is saying, "We could pay you a dividend, but we think it's better for you in the long term if we reinvest the money in the business now." That will lead to bigger growth and more profits in the long-term, and that'll mean even bigger dividends, even bigger share price rises for you, as long as you hang in there and stay invested.

That's all fine, but the fact that you're reinvesting profits and the fact that you're buying at a relatively expensive price in the first place means that growth investing is often riskier than value investing, but it can work very well. I mean, it worked especially well in the late 90s, where we saw a lot of technology companies perform really well, people like Dell and Microsoft and Amazon. But do bear in mind, it's not just technology companies that are growth companies.

Hargreaves Lansdown here in Britain over the last few years has grown at a phenomenal rate as a company, an amazing business. It's also done really well for shareholders. And yet, just about any time since it's been listed on the stock market, if you tried to value Hargreaves Lansdown on a price/earnings ratio, it's looked expensive. But because the business has been doing so well, actually the share prices carried on going up and investors have still done well.

One last thing I'd say is it's not always the case with growth companies that you're buying in high, you're buying at an expensive price. Normally that is the case but occasionally you'll get really lucky where you'll be able to see a growth company that is set to grow really fast over the next ten or 20 years. Actually the share price right now is remarkably low. You're almost then getting a win-win, where the share looks cheap now yet it still is going to grow at a fantastic rate.

What about value investing?

Value investors, they're often looking for companies where the market value, the share price is lower than the intrinsic value of the business. But again, just like buy low, sell high, that sounds great but it's easier said than done.

How do you identify the businesses where the market value is below the intrinsic value? Well, value investors often look at the dividend yield. If a company is paying a yield of 4%, 5%, 6%, that's a good value signal. They'll also look at the company's net assets - its property, also its intellectual properties, its trademarks, its patents, any holdings it has in other companies. If the net assets of the company are greater than the company's market value, greater than its share price, that is potentially a great value play. We often measure that using the price book ratio. Book is really just another word for net assets.

So, we want to have a company where the share price is either below book value or not that much above it. That's a good value signal. Do be careful though. Sometimes, with shares that look like good value shares, the market may be right. The company is cheap for a reason and you may be getting sucked into what we call a value trap.

So why do you get these value traps? Well, often it's because the business is facing big structural problems.

Right now, we think of regional newspaper companies. Obviously their market is contracting rapidly. You might find a regional newspaper company that looks cheap on the yield and on the net assets and on its price book ratio. But if the business is contracting fast, that, in the end, is the most important thing, and you as an investor may lose out, not be a big winner.

So, what should you do now in 2014? Should you be a value investor or a growth investor? Well, we're five years into the current stock market cycle. Share prices have had a good run, and you'd normally say, "That's a good time to be in value stocks rather than growth stocks." But I'd be a bit careful. For one thing, I think we should all be long-term investors. So, you don't want to get too worked up about where we might be in a five or seven-year cycle. We're thinking over 10 or 20 years.

The other thing to bear in mind is the current cycle is quite unusual. The financial crisis was obviously extraordinary. The banking sector is still behaving in a rather unusual way. So, the usual rules about stock market cycles and going in value stocks or growth stocks may not apply this time around. For me, I just say I'm not a worry about value or growth. I'm investing for the long-term. Some of the stocks will be more like growth stocks, stocks that I would think will grow for many years to come. Some of my investments are more like value investments that look cheap on several metrics. I mean, there aren't that many of those at the moment, but I'm always out there looking for them, along with the good growth stocks.

So, I'm doing growth investing, I'm doing some value investing, and I'm also investing in the market as a whole, because I know that stock markets normally go up over the long-term. I'm investing in markets as a whole, using index trackers, using passive ETFs. If I take that easy, simple stock market approach, I don't really need to worry about growth or value investing. I'm just investing in the market.

So, that's all I've got time for this week. I'll be back with another video soon. Until then, good luck with your investing.