Equity crowdfunding: you can invest in start-ups

In this video, Ed Bowsher explains how equity crowdfunding works as well as the risks and opportunities.

Equity crowdfunding is all the rage at the moment. This new phenomenon enables ordinary people to browse start-up companies on a crowdfunding platform, and then invest in some of them if they wish.

In this video, I explain how equity crowdfunding works as well as the risks and opportunities.

Transcript

How are you going to do this? You're going to do this by something called crowdfunding', which you may have heard of. It's very trendy at the moment and it's a big growth area. What exactly is crowdfunding and how does it work?

Try 6 free issues of MoneyWeek today

Get unparalleled financial insight, analysis and expert opinion you can profit from.

Sign up to Money Morning

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

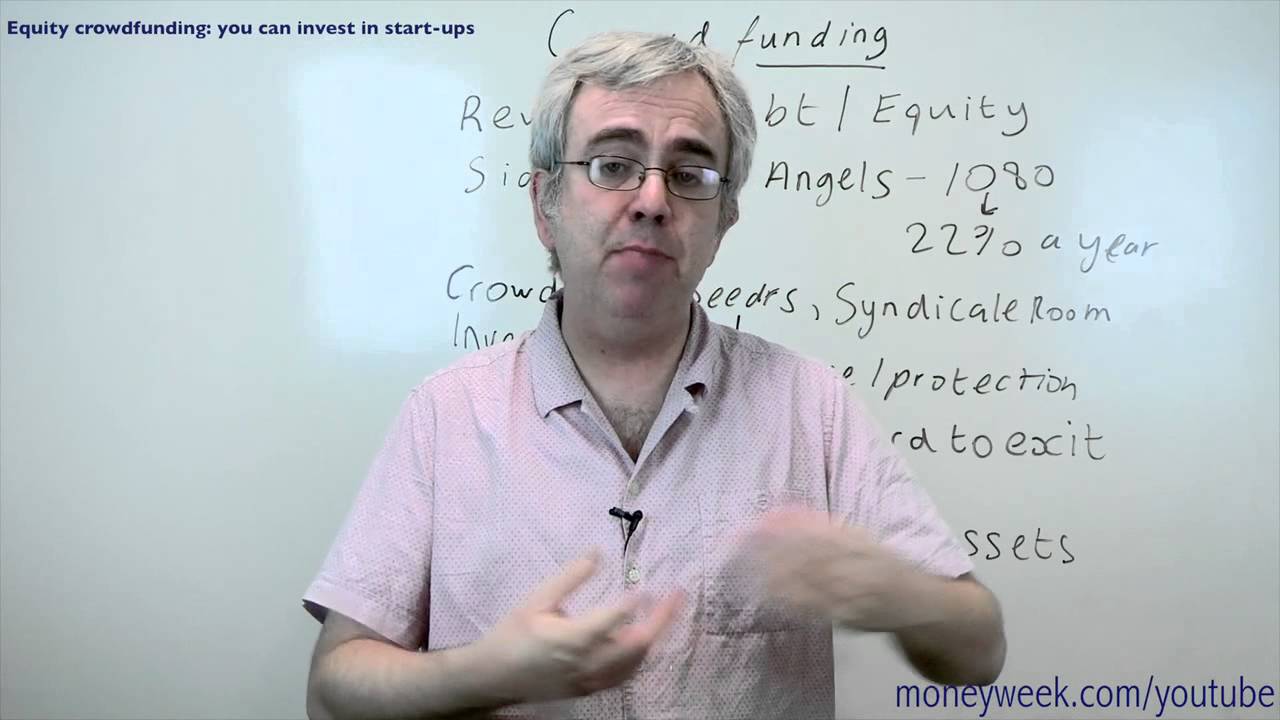

There are three main types of crowdfunding: we've got reward crowdfunding, debt crowdfunding, and equity crowdfunding.

Reward crowdfunding, you'll find that on sites like Indiegogo and Kickstarter. This is where you invest money in a business or give money to someone just doing a project maybe an art project. Whatever it is, you're really donating to that project and not investing.

In return, you'll get some sort of gift or reward from the business or project. That could be a T-shirt or whatever that project is trying to produce.

Personally, I'm not terribly interested in reward crowdfunding. I want real shares in a business. I've got enough T-shirts, thank you very much.

Then, we've got debt crowdfunding which is pretty much as it sounds. It's where you normally lend money to a business perhaps by a conventional loan or maybe you're buying bonds issued by that business.

I think the best known website in the debt crowdfunding space is Funding Circle. I know that quite a few 'MoneyWeek' readers have lent money via the Funding Circle website, and they've got quite decent interest rates in return.

Now, that's all the time I have for debt crowdfunding, because I really want to focus on equity crowdfunding'. This is where you invest money in a young business or a start-up and you get real shares in return.

You're getting the excitement of getting into a business on the ground floor, and maybe, who knows, that business could grow and become the next big Facebook or whatever it is, and you could be making profits of 10,000% or 20,000%, crazy, crazy money, crazy, crazy profits.

Of course, that's not going to be the case in most businesses. Very few businesses become global superstars. But, even though that's the case, I think you can make a decent profit from equity crowdfunding if you have a bit of luck and you go about it the right way.

There was a report done a few years ago called "Siding with the Angels". It looked at over 1,000 companies that started up in the UK between 1998 and 2008, and if you'd invested in all 1,080 of those companies, you'd have got an average annual return of 22%. That's a 22% per year return. Pretty good.

The trick there was to diversify, to invest across a wide range of businesses. It's inevitable that a lot of these businesses will go bust, so you just hope that a few of them will do well, and overall, you'll make a profit.

There are quite a few sites now out there that are equity crowdfunding platforms. The best known is probably Crowdcube. We've also got Seedrs, SyndicateRoom, InvestingZone, and a few others.

The way it works is very simple. Let's say you're an entrepreneur and you want to start a business. You go to one of the platforms, say to Crowdcube, and you get your business up on the site, and you say I'm looking for £50,000. You're going to have a time period of 60 days. You're looking for people to invest in your business during that 60-day period.

If you're not an entrepreneur, but an investor, you can invest as little as £10 or £20 in this business over that 60-day period. You'll see the amount of money growing as more and more investors come on board. Hopefully, it reaches the £50,000 target at the end of the 60-day period and then you've invested in the business.

If they don't get to the £50,000 target, or whatever the target may be, it might be a million it might be £10,000 if the target isn't reached, that investment is over and you get your money back. The company, the entrepreneur, hasn't got any money, and he has to think again about how he's going to raise some money.

In many ways, these sites are pretty similar. I think it's fair to say that Crowdcube is the number one site these days. It's got the most number of entrepreneurs looking for investment it's raising the largest amounts of money.

Seedrs is also doing well, as is SyndicateRoom, which is slightly different. The minimum investment on SyndicateRoom is £1,000. It's much lower on Seedrs and Crowdcube.

I'm probably a bit biased toward Seedrs, purely because I own a very small amount of shares in the business behind the platform. If the business does well, obviously, I may make some money in the long term.

Another reason why I'm very pro-Seedrs is I like its nominee structure. If you're an entrepreneur and you raise money on the Seedrs platform let's say the new shareholders own 10% of the business you founded Seedrs will manage that structure as the nominee of all the individual shareholders.

I think that's good for the entrepreneur. It makes it easier as he's only got to deal with one person Seedrs as the nominee for the individual investors.

It's also good news for the investors, because it means that Seedrs can really keep an eye on things and make sure that the interests of these early-stage individual investors are properly protected.

Just think about how this process will go, how it will work over the next few years. The entrepreneur might raise £100,000 on the Seedrs platform. Then, a year later, he might come back and raise another £100,000.

Then, the business grows. He could a year later go to one of the big venture capital firms and raise, say, a million pounds from the venture capital firm.

Of course, the venture capitalists will get a sizable shareholding in the business, and the early-stage investors who invested via Seedrs, their shareholding will be diluted. Instead of owning 10% of the company they might own, say, 5%.

That's fine. Dilution is absolutely something you should expect. It's not unreasonable. But, you need to be clear that the early-stage shareholders won't get badly treated, that they won't be hit by an unreasonably large dilution and their interest won't be damaged in some other way.

You need to trust the platform to make sure your interest will be looked after. I think Seedrs are especially aware of this issue and are the most likely to protect the interest of early stage investors.

Of course, the other big point to make here is if you do invest via equity crowdfunding, it's very high-risk stuff much higher risk than investing in shares via the stock market.

You've got the risk of insolvency. You might invest in 20 companies, and they could all go bust. That wouldn't surprise me. Hopefully, they won't all go bust. Maybe 12 will go bust, five will do OK, maybe two or three will do well, and overall you'll make a decent profit, but no guarantees. It might not work out that way.

Even if things do pretty well, it can be hard to exit. You may not be able to sell your shares for a while, because there's no secondary market. There's no stock market where you can just ring up a broker and say "I want to sell my shares".

Then, there's the risk of dilution that I already touched on. The size, the percentage stake that you own will probably fall a lot over the next few years.

The regulator, the FCA (Financial Conduct Authority), is very aware of the risks, so it says that the only people who should invest in equity crowdfunding are sophisticated investors, or high net-worth investors, or people who say that they won't put more than 10% of their investable assets into crowdfunding. Investable assets are all of your assets except your main home.

Frankly, I think 10% is probably too much. This is high-risk stuff. There's no way I'll invest as much as 10% of my investable assets in crowdfunding. I've already made a few crowdfunding investments. I'll probably make some more, but I think my absolute peak would be 5% of my investable assets in crowdfunding. It's just too risky to put any more money than that in.

That's a really quick overview on equity crowdfunding and how you can invest in a young start-up business. I hope you found it useful. I'll be back with another video soon. Until then, good luck with your investing.