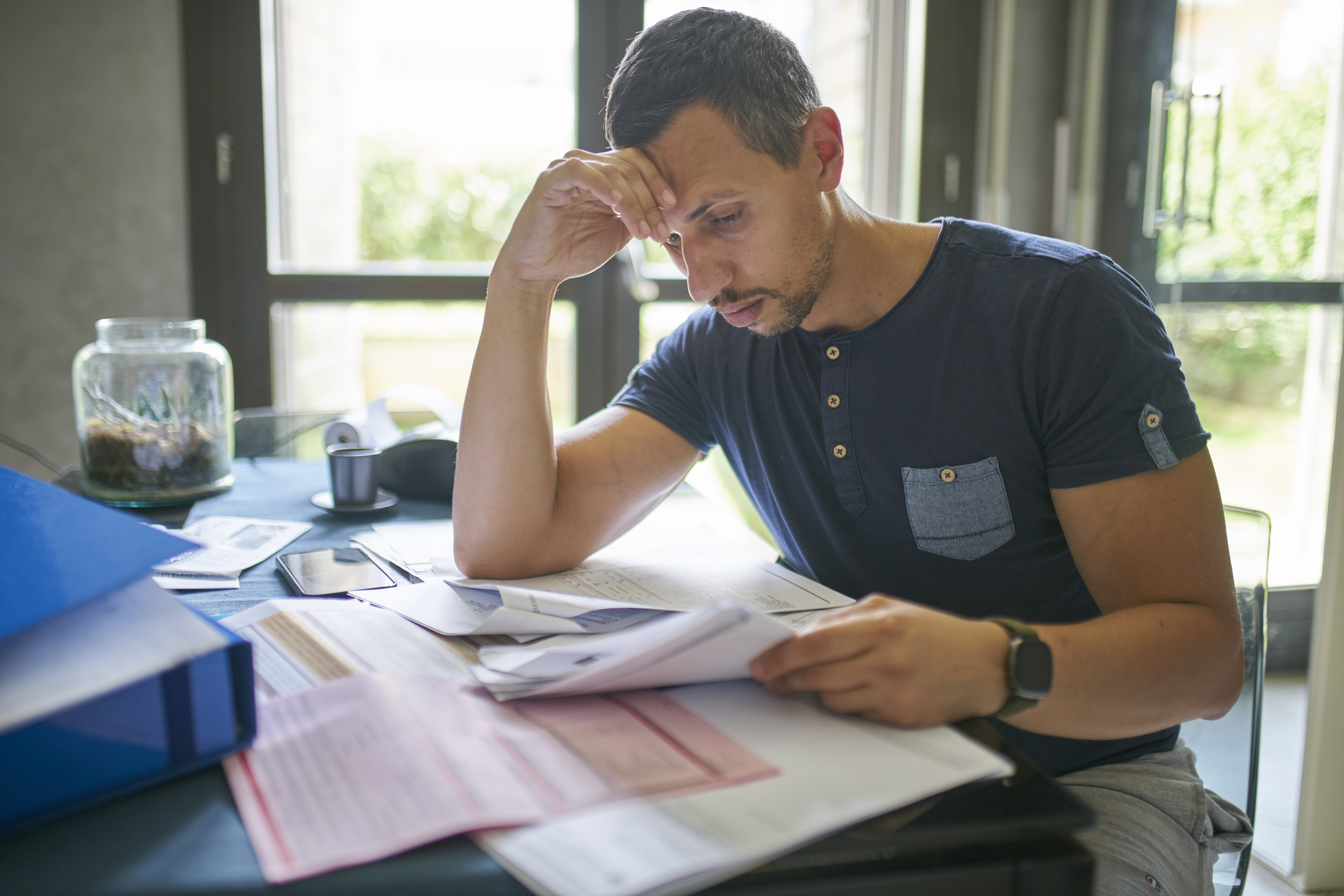

Don’t miss 31 July ‘payment on account’ tax deadline

Many self-employed people have a second tax payment deadline. With an 8.25% interest charge on late payments, it’s important to pay your bill on time

You are now subscribed

Your newsletter sign-up was successful

Want to add more newsletters?

Twice daily

MoneyWeek

Get the latest financial news, insights and expert analysis from our award-winning MoneyWeek team, to help you understand what really matters when it comes to your finances.

Four times a week

Look After My Bills

Sign up to our free money-saving newsletter, filled with the latest news and expert advice to help you find the best tips and deals for managing your bills. Start saving today!

Self-assessment taxpayers who need to make their second payment on account for the 2024/25 tax year have less than two weeks to do so or face hefty interest charges and penalties.

Workers who make payments on account must do so by midnight on 31 January and 31 July every year.

The deadline applies to all those who are self-employed unless they owe £1,000 or less (as this can be made in a single payment on the first tax return), or they have already paid more than 80% of the tax they owe.

MoneyWeek

Subscribe to MoneyWeek today and get your first six magazine issues absolutely FREE

Sign up to Money Morning

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

Don't miss the latest investment and personal finances news, market analysis, plus money-saving tips with our free twice-daily newsletter

What is payment on account?

Many self-employed people are required to make two payments on account each year. HMRC works out an estimate for what your tax bill is likely to be, based on previous tax years, and splits this into two payments on account.

So on 31 January, not only will you have to pay your tax bill for the 2023/24 tax year, you also have to pay your first payment on account for the 2024/25 tax year. The second payment on account then needs to be paid by 31 July.

You can request for your payments on account to be lowered if you believe your income will fall and you will therefore be liable for a smaller tax bill.

The tax can be paid online using a debit or corporate credit card; or via bank transfer, direct debit or a cheque in the post – however, plan this in advance to avoid any transfers being received after the deadline.

For those who still receive paper statements from HMRC, it’s also possible to make the payment at your bank or building society.

Penalty interest rate rises

The amount of interest HMRC charges on income tax not paid on time was recently upped, making it more vital than ever to pay your outstanding tax by 31 July.

From April 2025, the government increased the late payment interest rates to 4% plus base rate, which saw the rate initially jump to 8.5%, the highest level since August 2007. The rate fell to 8.25% at the end of May to take into account the latest Bank of England interest rate cut, and remains at that level.

The interest on late payments was previously set at 2.5% over base rate.

The tax authority saw receipts for interest on overdue payments jump from £147 million in 2021-2022 to £252 million in 2022/23, according to a Freedom of Information request submitted by financial advisory firm NFU Mutual.

Sean McCann, chartered financial planner at NFU Mutual, comments: “The change in April saw the interest on late tax payments rise to 8.5%. Even with the recent reduction in the base rate, an interest rate of 8.25% is a heavy charge on taxpayers who pay late.

“Late payment interest accrues daily from the date the payment is due, so this increase makes it even more crucial to pay your tax on time.”

Trott adds: “Given the potential cost of delay, it’s essential that individuals check their self-assessment account now and act ahead of the 31 July deadline. While long-standing self-employed individuals are likely to be familiar with these deadlines, they can easily catch out those newly self-employed who’ve submitted their first return this year.”

'Do I have to file a self-assessment tax return?'

About 12 million people are expected to file a self-assessment tax return each year. While it is predominantly seen as something that self-employed workers have to do, there are many people in regular employment who are also required to file a tax return.

It largely comes down to whether you receive some form of income that is not taxed at the source. As a result, alongside the self-employed, those who receive an income from renting out property or who make large amounts of money from investments (which aren’t held in an ISA) will also have to file a return.

So too will those who need to pay capital gains tax after profiting from the sale of an asset, or who earn an income from abroad.

Other examples include people that earn more than £60,000 and need to repay some of the child benefit they have received, and higher or additional-rate taxpayers who want to claim extra tax relief on their pension contributions.

About 97% of people filing a tax return choose to do so online, while 4% submit a paper return.

Registering to file a self-assessment tax return

You need to register with HMRC in order to file a self-assessment tax return. This must be done by 5 October for the following tax year.

You can do this online through the Gov.uk website, after which you will be sent a unique taxpayer reference through the post. Activation details for the government’s Gateway platform will also be posted to you; the Gateway is used for filing an online tax return.

This process can take up to three weeks, so it’s a good idea to start the registration process as early as possible.

Filing your self-assessment tax return and paying your tax bill

You have until 31 January to file your self-assessment tax return and pay your tax bill, if you’re doing it online.

This deadline is for the previous tax year. So you have until 31 January 2026 to file your tax return and pay your bill for the 2024/25 tax year.

Those who file their tax return by paper have to send it in by 31 October – although the deadline to pay any tax due is still 31 January.

Once you have completed your tax return, and HMRC has told you how much tax you owe, you have a few different payment options for clearing your tax bill.

Many taxpayers opt to pay the bill in full through a single lump sum payment, but there are various ways in which you can do that. A single payment could be made using a debit card, for example, while you can also use a corporate debit or credit card, though this will incur a fee.

You can make the payment through your online banking service to the HMRC bank account. You can also make a payment from your bank or building society’s local branch, or by posting a cheque to HMRC.

These payments can take a few days to go through, so it’s good advice to make the payment in advance of that deadline.

It’s not possible to pay at the Post Office anymore.

The penalties for late tax returns

A £100 penalty fine will be levied if you are late in filing your tax return and paying your bill - with more fines after that if you fail to pay.

This penalty is increased if you are more than three months late. You will also have to pay interest on the money owed.

McCann notes: “A penalty of 5% of the tax due is normally charged 30 days after the due date.

“An additional 5% penalty is charged on sums outstanding after six months with a further 5% penalty on any tax outstanding twelve months after the due date.”

However, HMRC has said it will not slap you with a penalty for 'honest' mistakes. It will accept certain excuses if you want to appeal against a penalty for a late tax return, including the death of a close relative, a spell in hospital, or if your computer fails.

If you are unable to pay, contact HMRC as soon as possible to see if a repayment plan can be put in place.

'What should I do if I make a mistake filing my tax return?'

If you have made a mistake with your tax return, you can correct it yourself within 72 hours. This can be done through the Gateway platform if you file your return online, while those who do their return through the post can download a new form to fill in. The word “amendment” needs to be written on every page.

After this date, you’ll need to write to HMRC to outline any errors made. You must make clear why you think the wrong amount of tax has been paid and how much you either owe or should be refunded.

You are able to claim refunds up to four years after a tax year ends.

Expenses if you are self-employed

You may be able to claim certain expenses when filing your self-assessment tax return, which will lower the size of your tax bill.

These could include office costs, such as for stationery or computer equipment, or travel costs, such as train fares.

Crucially, these need to be expenses that are the result of you carrying out your job ‒ you can’t claim for a laptop which you are actually using for leisure purposes, for example.

You may also be able to claim towards a portion of certain household expenses, should you work from home, such as your energy bill. You cannot deduct the entire bill ‒ instead you will be required to work out what portion of your energy use is the result of your work.

An easier option is the simplified expenses scheme, which allows self-employed people to claim a flat rate. This is determined by the number of hours they work from home each month and ranges from £10 to £26 a month. You will need to work at least 25 hours a month from home.

High Income Child Benefit Charge

One reason for some people needing to file a self-assessment tax return is so they can pay the High Income Child Benefit Charge.

The charge is levied against people who earn more than £60,000 a year, and acts as a taper, gradually claiming back the child benefit paid to such high earners.

The benefit is effectively withdrawn at a rate of 1% for each £200 earned over £60,000 a year by the higher-income partner. Therefore, child benefit is fully withdrawn where the adjusted net income of the higher-income partner reaches £80,000 a year.

The partner who earns the highest amount is responsible for paying the High Income Child Benefit Charge, even if they are not the one that receives the child benefit payments.

'I'm struggling to pay my tax bill. What are my options?'

According to Trott at St. James’s Place, if you find yourself unable to pay what you owe, it’s important to contact HMRC as soon as possible.

She comments: “While it may be tempting to delay or ignore the issue, HMRC does consider reasonable excuses, and reaching out early gives you the best chance of avoiding escalating penalties.

“For anyone simply caught off guard by this month’s deadline [on 31 July for payments on account], now is also a good time to think about how to be more prepared going forward, whether that’s setting aside funds on a regular basis or setting up a Budget Payment Plan with HMRC.”

Some taxpayers who are unable to pay the bill off in full can look to set up a ‘Time to Pay’ arrangement. For some this can be done online, but in other cases you may need to discuss your needs with HMRC staff directly. As the name suggests, Time to Pay allows you to pay the bill off over a longer period, in instalments.

HMRC will look into your financial arrangements to work out how much money you have left each month after the essentials, such as food and utility bills, have been paid. It can then calculate what you can afford to pay towards the bill.

For some taxpayers, the bill can be paid through their tax code. This is not an option for everyone ‒ you can only do this if you owe less than £3,000 and already pay tax through pay as you earn (PAYE), for example because you are employed in some capacity rather than entirely self-employed. You will also have to have submitted either a paper tax return by 31 October or an online tax return by 30 December.

Finally, as Trott mentioned, it’s possible to make regular payments towards the next year’s tax bill by putting a Budget Payment Plan in place. With such a plan, you make payments on either a weekly or monthly basis, which are directed towards your next bill.

It means that when you actually file your tax return, you can then either claim a refund or top up the payments to clear the amount you owe.

With all of your self-assessment tax return payment methods, it’s important to note down your UTR. You will need to include this as a reference, for example when making an online payment, or by writing it on the back of the cheque. This means that HMRC is able to easily work out which tax bill the money is meant to go towards.

-

Average UK house price reaches £300,000 for first time, Halifax says

Average UK house price reaches £300,000 for first time, Halifax saysWhile the average house price has topped £300k, regional disparities still remain, Halifax finds.

-

Barings Emerging Europe trust bounces back from Russia woes

Barings Emerging Europe trust bounces back from Russia woesBarings Emerging Europe trust has added the Middle East and Africa to its mandate, delivering a strong recovery, says Max King

-

Two million taxpayers to be hit by £100k tax trap by 2026/27

Two million taxpayers to be hit by £100k tax trap by 2026/27Frozen thresholds mean more people than ever are set to pay an effective income tax rate of 60% as their earnings increase beyond £100,000. We look at why, as well as how you can avoid being caught in the trap.

-

13 tax changes in 2026 – which taxes are going up?

13 tax changes in 2026 – which taxes are going up?As 2026 gets underway, we look at what lies ahead in terms of changes to tax rates and allowances this year and how it will affect you.

-

How to limit how much of your Christmas bonus goes to the taxman

How to limit how much of your Christmas bonus goes to the taxmanIt's Christmas bonus season but the boosted pay packet may mean much of your hard-earned reward ends up with HMRC instead of in your pocket

-

Over 1 million pay 45% rate of income tax as fiscal drag bites

Over 1 million pay 45% rate of income tax as fiscal drag bitesHundreds of thousands more people are being pushed into the additional rate tax band by fiscal drag

-

'I've used my annual ISA allowance. How can I shield my savings from tax?'

'I've used my annual ISA allowance. How can I shield my savings from tax?'As millions face paying tax on savings interest, we explore how to protect your money from the taxman. If you've used up your ISA allowance, we look at the other tax-efficient options.

-

Simple assessment explained as millions brace for unexpected tax bills

Simple assessment explained as millions brace for unexpected tax billsIncreasing numbers of people could get letters from HMRC saying they owe more tax due to frozen thresholds, under a system known as simple assessment. Here is what it means for you.

-

What are wealth taxes and would they work in Britain?

What are wealth taxes and would they work in Britain?The Treasury is short of cash and mulling over how it can get its hands on more money to plug the gap. Could wealth taxes do the trick?

-

When is the self-assessment tax return deadline?

When is the self-assessment tax return deadline?If you are self-employed, rent out a property or earn income from savings or investments, you may need to complete a self-assessment tax return. We run through the deadlines you need to know about